Are Brick-and-Mortars Starting To “Get” The Web?

Written by Evan SchumanA major E-Commerce customer satisfaction survey is showing traditional brick-and-mortar retailers quickly catching up with the traditional pureplay Web retailers.

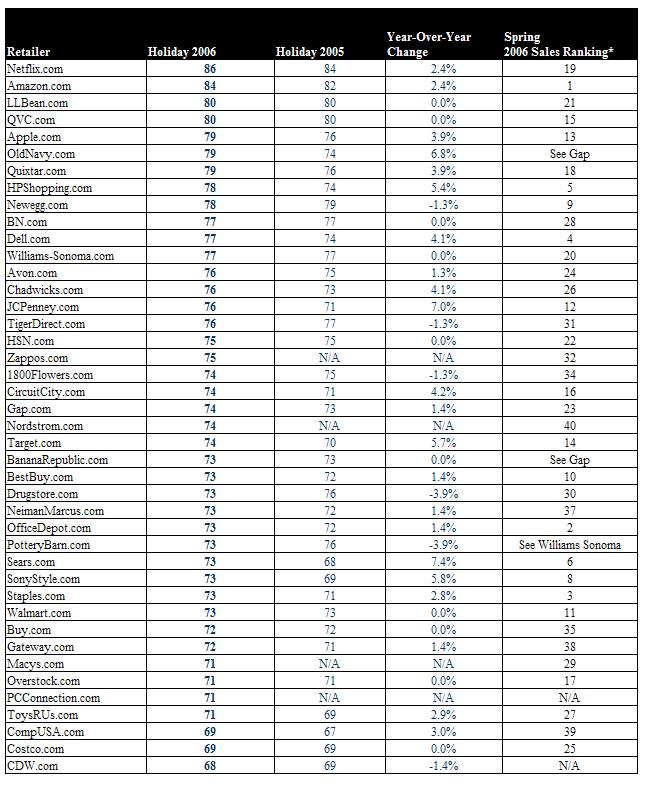

Although the figures released this week by ForeSee Results still show the same players safely on top?including Netflix, Amazon.com, LLBean.com, QVC.com, Apple.com and Old Navy.com?and the same players (including Costco, CompUSA and CDW) on the bottom, ForeSee CEO Larry Freed sees surprising advances by some of the at-one-time Web challenged multi-channel retailers.

“They’re definitely gaining ground and really stepping up. It’s encouraging to see,” Freed said, specifically noting that “JC Penney (+7 percent), Sears (+7.4 percent) and Target (+5.7 percent) all racked up huge improvements from last year?s holiday satisfaction scores.”

There are several reasons for this change, but the primary one is that brick-and-mortar execs are starting to appreciate the value of E-Commerce beyond its direct revenue. In other words, Freed argues that some execs are starting to understand that some site visitors will buy in-store, which means that Web sites are increasing sales, but those increases are not necessarily materializing as Web sales.

As more customers shop online and then pick up instore (to see and touch merchandise and to receive it immediately while avoiding shipping charges) and more customers do the reverse (Freed said he recently shopped in-store for a large television but purchased it online so that it could more easily be shipped), top retail execs are start to appreciate the new world.

Another possible cause is that some pureplays are getting into so many different areas that they may be distracting themselves. Amazon’s continuing efforts to sublease its site to other retailers (whose shipment, return and other policies may be quite different from what customers expect at Amazon) as well as move into other areas (such as selling space on its servers) could easily distract the E-Commer giant.

The primary cause, though, is the secondary financial benefits of E-Commerce operations. In a strict revenue sense, few online units of traditional brick-and-mortars are delivering much more than 7 percent of global revenue. But when other items?such as more sophisticated customer data in addition to the offline referrals?are factored in, the online unit can be much more important.

Freed said the brick-and-mortars still have a long way to go and added that many are still clinging to compensation and incentive packages that tend to pit online against offline, but he’s seeing progress.

“Over the years, I’ve seen a transformation in the language. It seems to be closing a little bit,” he said, adding that one approach is to incentivize managers based on any sales within their geography. That will push offline and online execs to drive sales the most efficient ways, regardless of channel.

This ultimately will require the often-sought-but-rarely-found single view of the customer. (Click to read an older profile of some nontraditional single-view-of-the-customer ideas from Limited Brands and its Victoria’s Secret line.)

On the one hand, such tracking methods exist, but the challenge is much greater than simply getting multiple databases to talk with each other (although that’s not so easy, either). In store, courtesy CRM cards are often forgotten or deliberately not used. Online, cookies are frequently deleted and many customers don’t want to register.

The only practical way around this will involve customer incentives, such as percent off purchases (both in-store and online) but only for registered users. Retailers will likely have to offer a lot more than convenience to get that integrated view, but there’s no way to measure the true influence of each channel without it.

Freed predicted that many retail execs will soon start to think creatively about shipping charges, factoring in storage and other inventory costs. “I actually believe there will be a point in time when shipping will be free across the board,” Freed said.

Another predicted change is universal pricing, where online and offline prices will be identical. “Consumers want the same product at the same price in both channels,” he said.

For the record, of the 42 top retail brands listed, only seven sites saw their satisfaction scores drop from last year’s survey: Newegg (-1.3 percent); TigerDirect (-1.3 percent); 1-800-Flowers (-1.3 percent); Drugstore.com (-3.9 percent); PotteryBarn (-3.9 percent); Drugstore (-3.9 percent); and CDW (-1.4 percent). The research was conducted using the methodology of the University of Michigan?s American Customer Satisfaction Index (ACSI) and surveyed more than 10,000 online holiday shoppers, according to ForeSee.

Cards issued by European banks when used online cross border don't usually support AVS checks. So, when a European card is used with a billing address that's in the US, an ecom merchant wouldn't necessarily know that the shipping zip code doesn't match the billing code.

Cards issued by European banks when used online cross border don't usually support AVS checks. So, when a European card is used with a billing address that's in the US, an ecom merchant wouldn't necessarily know that the shipping zip code doesn't match the billing code. -Marc

-Marc

{kind=link}